Back

Smartphone adoption is rapidly increasing, particularly among youth and lower-middle-class urban populations. However, a significant portion of consumers cannot afford to pay the full price upfront. While demand is high, access to credit remains limited due to the absence of formal banking histories for most buyers.

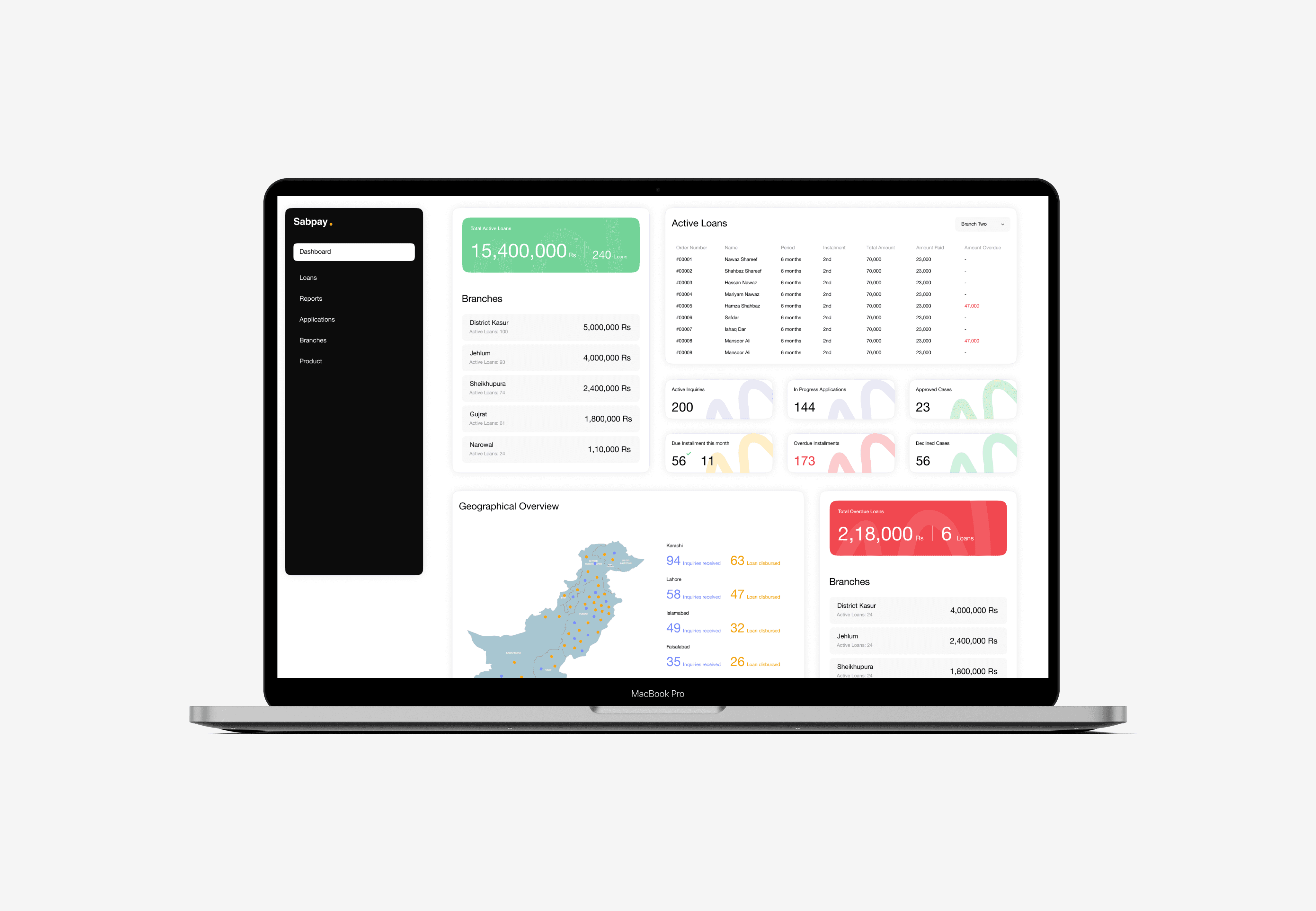

SabPay is a fintech startup addressing this gap through a micro-lending mobile application that enables customers to purchase smartphones via easy monthly installments with minimal documentation, powered by digital credit scoring.

Developed by Txend, the platform facilitates the digital transformation of Buy Now, Pay Later (BNPL) vendors. It is purpose-built for BNPL organizations with multiple branches, offering low-income households access to essential goods through manageable, interest-free installment plans. This approach helps customers avoid high-interest debt while acquiring necessary items.

Currently, the focus is on smartphones, but the solution is designed for future scalability to include other essential products. By digitizing operations and streamlining sales, SabPay empowers vendors with clarity and data-driven insights for informed decision-making

Challenge

Before the digital transformation, SabPay relied on paper registers and manual file systems across multiple branches nationwide. This outdated system led to numerous operational challenges. Record discrepancies became common due to inconsistent and incomplete data, stemming from a lack of centralized coordination. Financial inaccuracies were also frequent, as rapidly changing information couldn’t be updated in real time. Additionally, the company faced limitations in credit assessment, particularly when evaluating the credit histories of unbanked and underbanked clients.

These inefficiencies extended to daily operations, where staff struggled to track tasks, manage cases, and meet performance targets. Scalability was another major hurdle, as manual processes made expansion difficult and resource intensive. Furthermore, the lack of transparency and proper verification protocols increased the risk of fraudulent applications, ultimately affecting the company’s reliability and trust. The need for a streamlined, digital solution became clear to support growth and operational efficiency.